Quicklinks

Top Results

2025 Annual Report

History was made here in 2025.

Here for today, here for your future

2025 was the year Civic leapt into the future, as a fully independent credit union. Innovative, fresh, forward-facing. All backed by a 43-year history of proven success.

We’re here to meet your needs today, and for years to come. The future starts now.

Watch this year's meeting

Watch the Annual Meeting video to see the installment of elected board members, get details on Civic's financial performance, and more.

Letter from our Board Chair

Dr. Aaron Noble

Dear members,

2025 was a historic time in the life of your credit union. For 43 years, we have proudly served as the only credit union dedicated to the North Carolina local government community, and we’re grateful for the work our members do to better our towns, cities, and state.

Our official transition to Civic from Local Government Federal Credit Union in 2025 represents a continuation of our commitment to you, while transitioning our independence as a modern financial institution.

David D’Annunzio

CEO Report

When I accepted the opportunity to serve as CEO of Civic, it was for one clear reason: purpose.

Civic exists to serve North Carolina’s local government employees, the people who keep our communities running every day. That focus remains constant. While many financial institutions broaden their reach, we remain committed to serving those who serve our state.

From my first days here, I have been inspired by the strength of a dedicated team, strong digital capabilities, and a culture grounded in professionalism and care. We are clear in our mission and positioned to evolve.

Impact Report

2025 was a year of impact, influence, and inspiration. See where and how we made our biggest and best impacts with the Civic 2025 Impact Report.

Tribute to Dwayne Naylor

Civic Credit Union’s President and Chief Executive Officer Dwayne Naylor retired in January 2026 after serving more than 40 years in the credit union industry. He had started with Local Government Federal Credit Union in 2000 and was appointed Chief Operating Officer in 2013 to launch and build Civic Federal Credit Union.

Dwayne’s hopes for Civic were inspired by his longtime involvement with the World Council of Credit Unions (WOCCU), which led him to see Civic through a wider, more future-forward lens. Dwayne’s focus on the "triple bottom line" — a sustainable enterprise that delivers economic, social, and environmental benefits — directed the Civic commitment to people, planet, and prosperity.

Rooted in the philosophy of doing well while doing good, Dwayne connected personally with many members and often handed out his cell phone number to continue the conversations.

Above all else, Dwayne was in step with the credit union mission. We are grateful for his stewardship and his leadership over the many years he served our members.

Civic Board of Directors

Our Board is experienced, committed, and elected by credit union members like you. These men and women set Civic policies, perform key audit functions, and appoint our CEO and members of the Supervisory and Loan Review Committees. And … they are volunteers.

Read more about each member of the Civic Board of Directors.

Dr. Aaron Noble, Chair

Burlington

David Dear, Vice Chair

Shelby

Tony Brown, Treasurer

Halifax County

Ruth Barnes, Secretary

Atlantic Beach

Lin Jones

Durham

Kellie Blue

Robeson County

Paul Miller

Snow Hill

Jeanne Erwin

Cary

Ken Noland

Wilkesboro

Supervisory Committee

This committee is tasked with inspecting Civic assets for security, its records for accuracy, and its procedures for the proper handling of credit union funds. Civic members who serve on the Supervisory Committee include:

Amy Bason

Raleigh

Ryan Draughn

Sanford

Emily Lucas

Wake Forest

Justin Merritt

Shelby

Shawn Purvis

Apex

Loan Review Committee

At Civic, members have the right to appeal a loan decision. When they do, this committee has the authority to review the decision, and choose to uphold it or approve the loan. Civic members who serve on the Loan Review Committee include:

Jim Baker

Chapel Hill

Diana Harris

Cary

Nancy Held

Raleigh

Pam Hurdle

Hertford

Dale Johnson

Raleigh

Nancy Medlin

Garner

Charles Murray

Louisburg

Jean Stowers

Surf City

Sam Tingler

Holly Springs

Charles Weber

Washington State

Mark Williams

Wake Forest

Civic Advisory Council

This group of collaborative and dedicated volunteers helps shape our credit union, advocate for their fellow members, and make us who we are. We’re grateful for their many contributions.

Financial Report

By the numbers

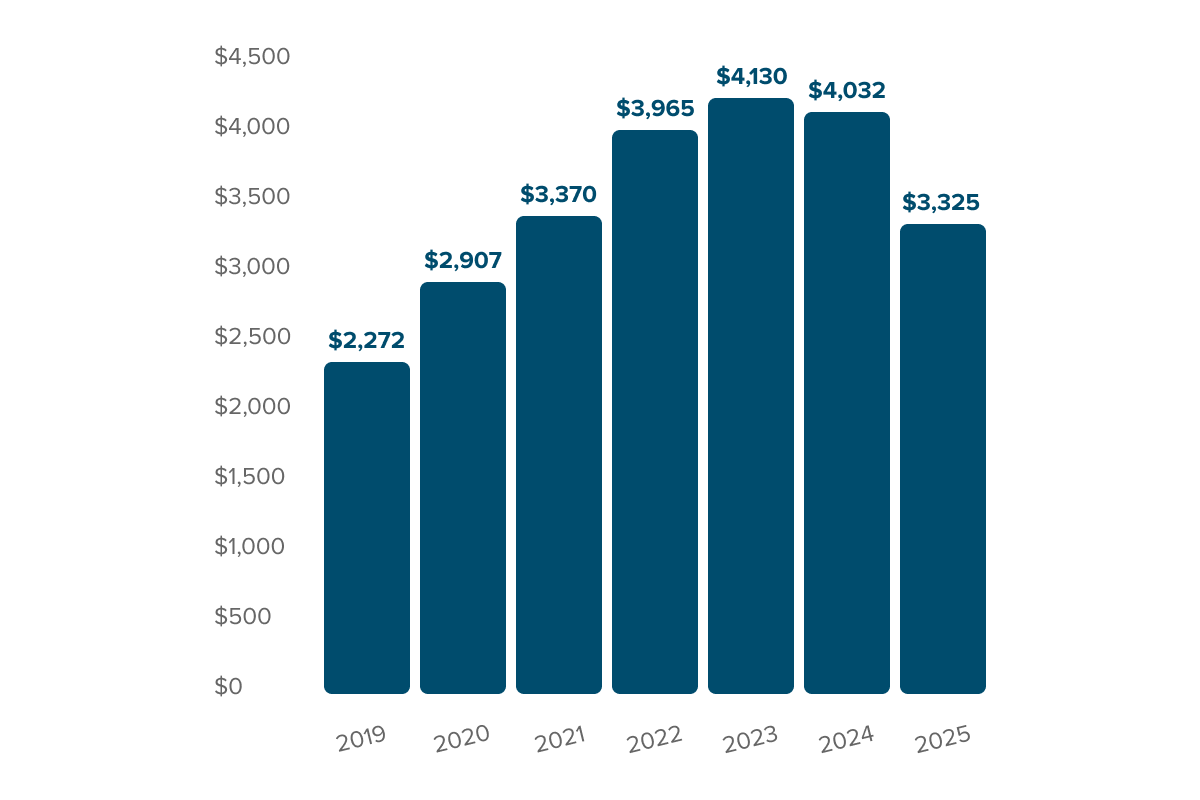

Asset growth

(in millions)

| 2018 | $2,074,000,000 |

| 2019 | $2,272,000,000 |

| 2020 | $2,907,000,000 |

| 2021 | $3,370,000,000 |

| 2022 | $3,965,000,000 |

| 2023 | $4,130,000,000 |

| 2024 | $4,032,000,000 |

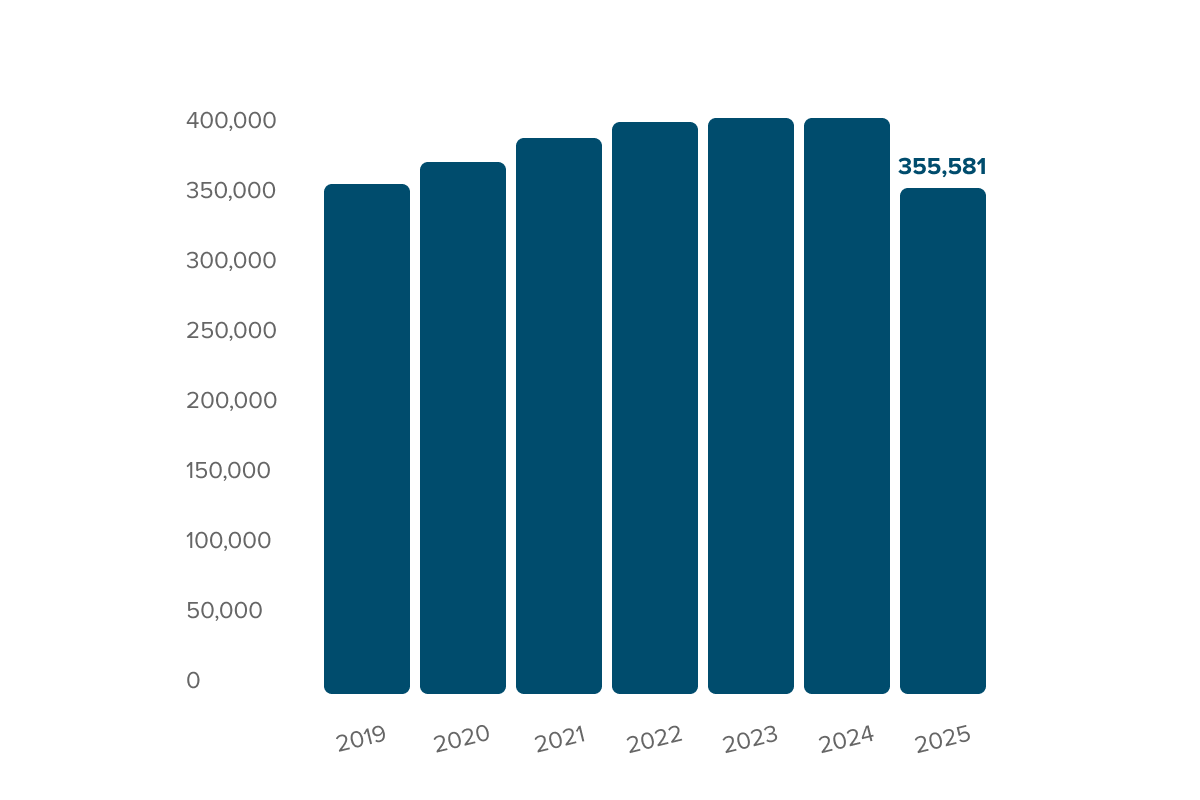

Membership growth

13% decrease in membership 2024-2025

| 2018 | $2,074,000,000 |

| 2019 | $2,272,000,000 |

| 2020 | $2,907,000,000 |

| 2021 | $3,370,000,000 |

| 2022 | $3,965,000,000 |

| 2023 | $4,130,000,000 |

| 2024 | $4,032,000,000 |

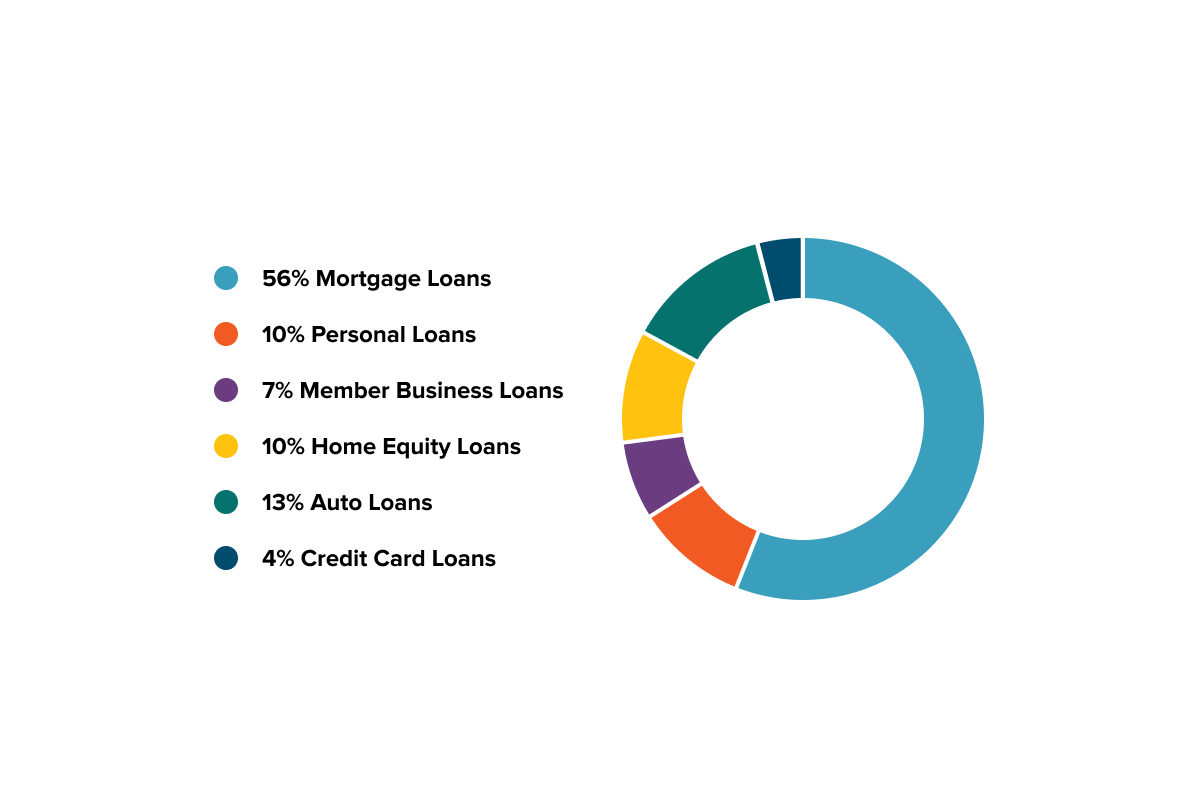

Loan portfolio mix

| Mortgage loans | 53% |

| Auto loans | 16% |

| Personal loans | 12% |

| Home equity loans | 9% |

| Member business loans | 6% |

| Credit card loans | 4% |

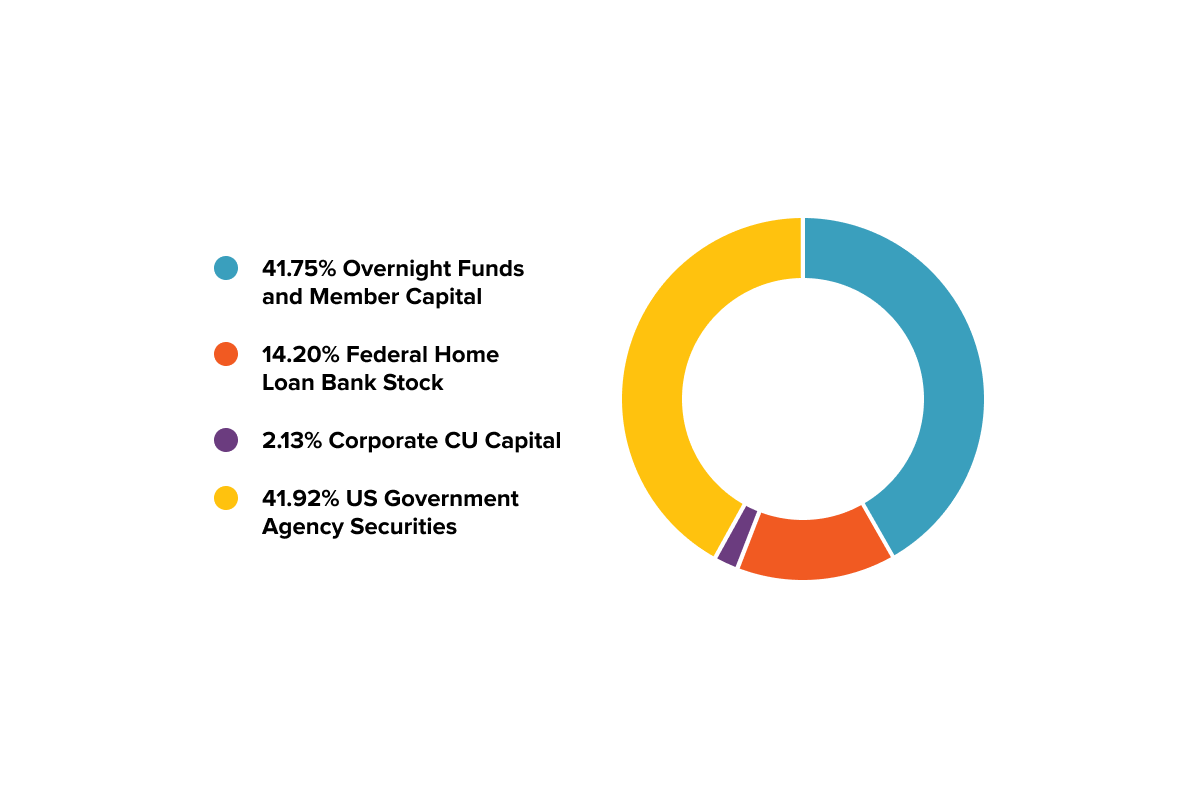

Investment portfolio mix

| Overnight funds and member capital | 64.46% |

| U.S. government agency securities | 29.92% |

| Federal Home Loan Bank Stock | 4.32% |

| Corporate CU capital | 1.30% |

Statements of Financial Condition

| 0 | Assets | 2025 | 2024 |

|---|---|---|---|

| 1 | Cash and Investments | $217,834,735 | $320,270,799 |

| 2 | Mortgage Loans | $1,648,777,786 | $1,877,088,030 |

| 3 | Personal Loans | $293,874,199 | $417,665,826 |

| 4 | Member Business Loans | $213,837,894 | $214,055,251 |

| 5 | Home Equity Loans | $305,634,115 | $318,873,374 |

| 6 | Auto Loans | $374,182,834 | $567,277,678 |

| 7 | Credit Card Loans | $120,023,127 | $152,619,062 |

| 8 | Allowance for Loan Losses | ($48,802,807) | ($51,044,257) |

| 9 | Net Loans | $2,909,941,122 | $3,496,534,965 |

| 10 | National Share Insurance | $26,838,773 | $33,747,490 |

| 11 | Other Assets | $170,396,365 | $181,644,692 |

| 12 | Total Assets | $3,325,010,994 | $4,032,197,946 |

| 0 | Liabilities & Equity | 2025 | 2024 |

|---|---|---|---|

| 1 | Payables | $604,170,279 | $126,784,823 |

| 2 | Share Accounts | $432,886,546 | $773,301,753 |

| 3 | Share Draft Accounts | $373,969,591 | $561,066,529 |

| 4 | Money Market Accounts | $511,003,423 | $841,952,629 |

| 5 | Individual Retirement Accounts | $102,455,038 | $184,355,242 |

| 6 | Share Certificates | $1,134,925,647 | $1,261,559,604 |

| 7 | Total Deposits | $2,555,240,246 | $3,622,235,756 |

| 8 | Total Reserves & Undivided Earnings | $165,600,470 | $283,177,367 |

| 9 | Total Liabilities & Equity | $3,325,010,994 | $4,032,197,946 |

Year to date as of 12/31/2025 and 12/31/2024.

Statements of Income

| 0 | Operating Income | 2025 | 2024 |

|---|---|---|---|

| 1 | Investment Income | $8,346,822 | $15,395,767 |

| 2 | Mortgage Loans | $69,384,707 | $77,949,121 |

| 3 | Personal Loans | $35,216,493 | $44,737,627 |

| 4 | Home Equity Loans | $22,456,315 | $22,005,703 |

| 5 | Auto Loans | $34,952,410 | $40,378,896 |

| 6 | Credit Card Loans | $17,858,996 | $21,185,013 |

| 7 | Member Business Loans | $8,872,941 | $8,192,773 |

| 8 | Total Loan Income | $188,741,863 | $214,449,133 |

| 9 | Other Operating Income | $49,146,544 | $63,549,255 |

| 10 | Total Income | $246,235,228 | $293,394,155 |

| 0 | Operating Expenses | 2025 | 2024 |

|---|---|---|---|

| 1 | Operating Expenses | $274,810,723 | $199,172,940 |

| 2 | Interest on Borrowed Funds | $13,824,567 | $9,984,211 |

| 3 | Share Accounts | $3,092,634 | $3,291,735 |

| 4 | Share Draft Accounts | $438,609 | $666,521 |

| 5 | Money Market Accounts | $13,769,230 | $17,473,562 |

| 6 | Individual Retirement Accounts | $4,046,341 | $4,399,025 |

| 7 | Share Certificates | $59,952,935 | $59,701,291 |

| 8 | Total Deposit Expense | $81,299,749 | $85,532,134 |

| 9 | Total Expenses | $369,935,040 | $294,689,286 |

| 10 | Net Operating Income | ($123,699,812) | ($1,295,131) |

Year to date as of 12/31/2025 and 12/31/2024.

Nature of operations

Civic Federal Credit Union (the “Credit Union”) is a not-for-profit cooperative that primarily serves employees of local government units. The Credit Union is organized under the laws of the Federal Credit Union Act and is exempt, by statute, from federal and state income and sales taxes. The Credit Union serves its members through Civic branches statewide and the nationwide CO-OP Shared Branch network. The Credit Union's primary source of revenue is its loan portfolio.

Audited financial statements

The financial reports provided here have not been audited. You can review audited financial statements for the annual period ending June 30, 2025, from the Credit Union's accounting firm, CliftonLarsonAllen LLP, posted in the Audit Report section. These financial statements include a more in-depth financial analysis and extensive footnote disclosures that provide additional information on the results of the Credit Union for the respective period ends as noted above. Open and view this current Audit Report in a separate tab outside of this document.